WASHINGTON, June 16 (Reuters) – Federal Reserve officials on Wednesday are expected to at least flag the pending start of talks about when and how to exit from the crisis-era policies the U.S. central bank put in place at the onset of the coronavirus pandemic last year.

With U.S. inflation rising faster than expected and the economy forecast to grow at its quickest pace in decades this year, some policymakers have begun questioning whether the Fed should continue to keep its benchmark short-term interest rate near zero and leave unchanged a massive bond-buying program put in place to stem the economic fallout from the pandemic.

Balanced against the improving economic terrain: The United States is still 7.5 million jobs short of where it was in early 2020, and the reopening of schools, concert venues and a host of other public areas remains a work in progress.

Daily coronavirus infections and deaths have plummeted, but only about half of those over the age of 12 have been fully vaccinated, short of what epidemiologists feel is needed to squelch the virus for good and eliminate the risk of future localized outbreaks.

Any actual change in monetary policy is, as a result, likely months down the road as the Fed balances a variety of risks.

The central bank’s latest policy statement, due to be released with fresh economic projections at 2 p.m. EDT (1800 GMT), is expected to err on the side of continuing the Fed’s support for the economy until more workers are back on the job. Fed Chair Jerome Powell is scheduled to hold a news conference to elaborate on the two-day meeting.

Yet enough has changed in recent months – and may start to change at an even faster clip – that analysts expect the Fed to at least acknowledge the start of policy discussions that will eventually lead to a plan to first reduce the monthly $120 billion in bond purchases to zero and then start raising interest rates.

“This is about getting the ball rolling,” in a process that may take months to complete, and in a way that avoids any rapid shift in sentiment among investors or consumers that could damage the recovery in the meantime, wrote Tim Duy, chief U.S. economist for SGH Macro Advisors and a University of Oregon professor focused on Fed policy.

LIFTOFF

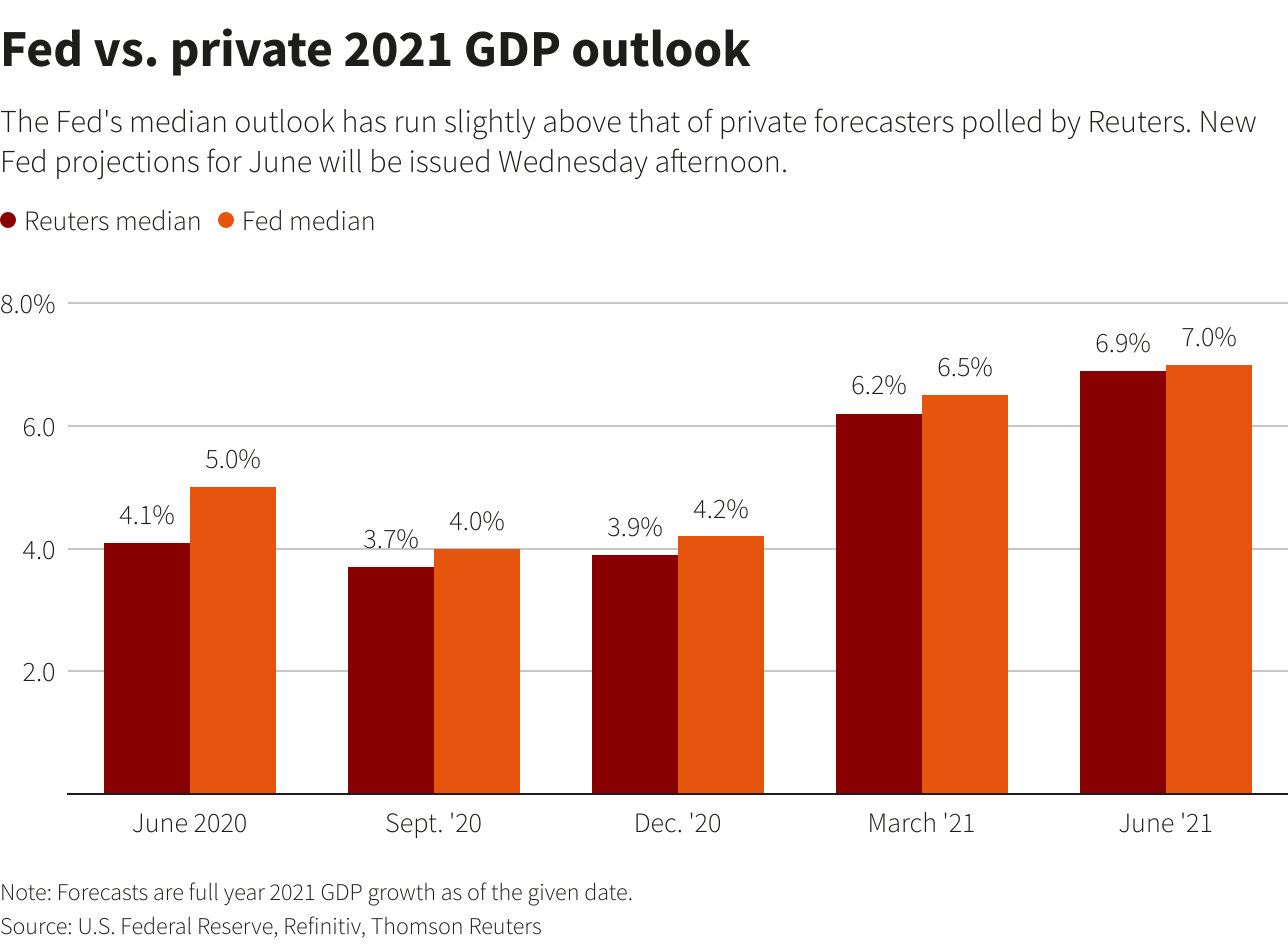

The new interest rate and economic projections will show just how much policymakers’ views have changed since March, when Fed officials at the median still projected the first interest rate increase would be delayed until at least 2024.

U.S. job growth has been weaker than expected in the intervening weeks, but inflation has run hotter – a worst-of-both-worlds outcome that has forced the Fed to bank on recent price hikes proving “transitory,” and hiring to accelerate as the nation’s economic reopening continues.

The Fed has laid out an explicit test for any rate hike – including the need for inflation to not just reach but exceed the central bank’s 2% target “for some time” in order to make up for years of inflation that was too low. The economy may only be at the start of that journey, even with the recent jump in the Fed’s preferred inflation measure to 3.6%. While that was the highest in 13 years, it was only one monthly reading and driven by factors officials feel will fade over time.

Still, the timing for the initial “liftoff” of rates could shift into 2023 if only two or three officials feel the improved outlook, or a too-fast-return of inflation, would warrant faster action – a change investors may read as particularly “hawkish.”

Deutsche Bank’s chief U.S. economist, Matthew Luzzetti, wrote last week that he felt it a “close call” whether the Fed’s updated “dot plot” of interest rate projections would advance an initial rate hike into next year, but that ultimately the policy-setting Federal Open Market Committee would see continued near-zero rates as more consistent with the path of the recovery and the management of the twin inflation and employment goals.

“With the labor market lagging, no strong evidence that the Fed’s transitory inflation story is incorrect, and market pricing moving closer to the Fed’s views on inflation and the policy rate, the Committee should not yet feel compelled to send a hawkish signal through their rates guidance,” Luzzetti said.